Get Started

Get started with Project: Risk Leader (PRL) by checking out these key resources.

Featured

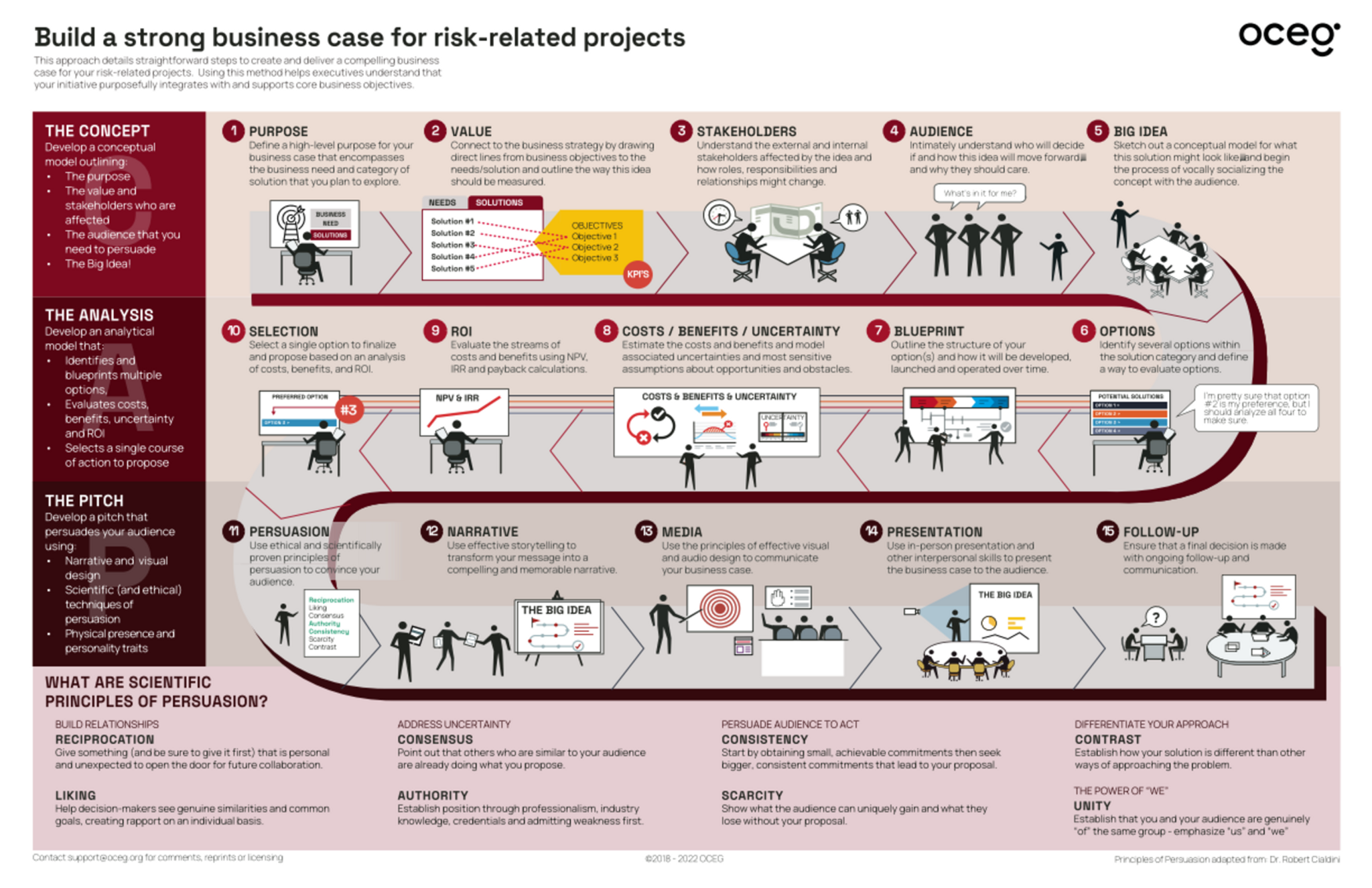

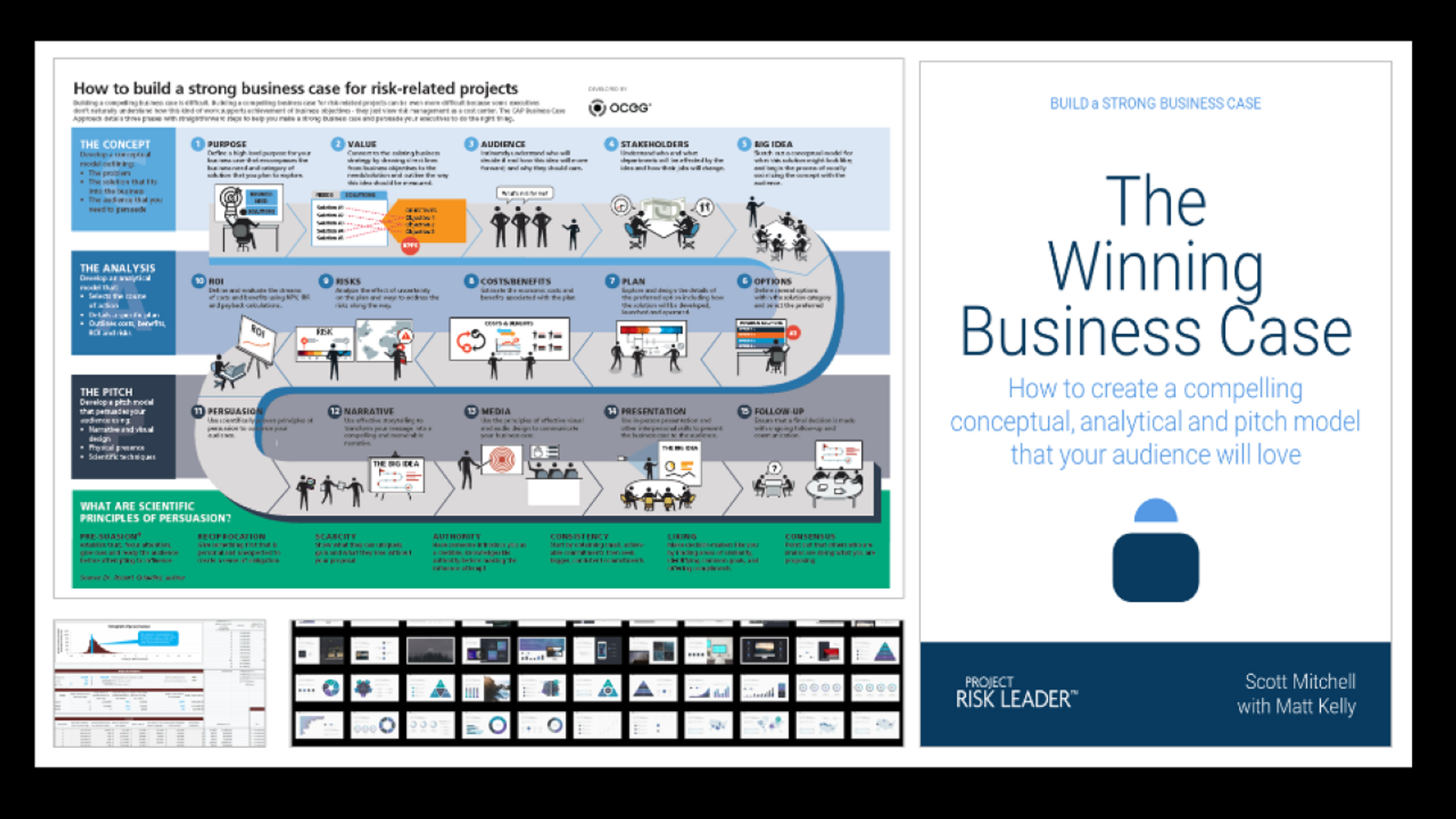

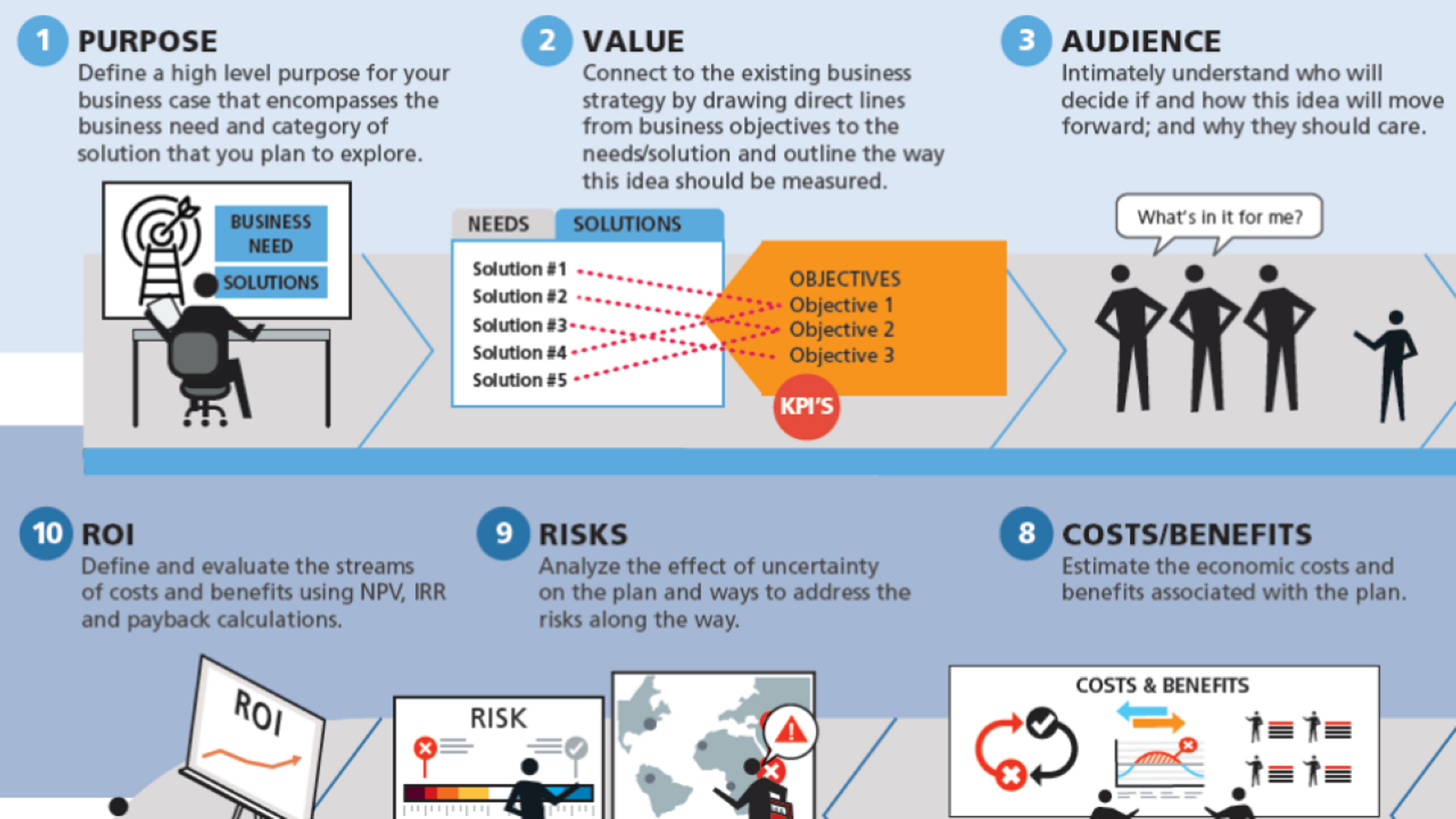

Making a Strong Business Case

Building a compelling business case is difficult. Building a compelling business case for risk-related projects can be even more difficult because some executives don’t naturally understand how this kind of work supports achievement of business objectives - they just view risk management as a cost center.

The Winning Business Case

This 100+ page book teaches you how to create a compelling conceptual, analytical and pitch model that your audience will love.

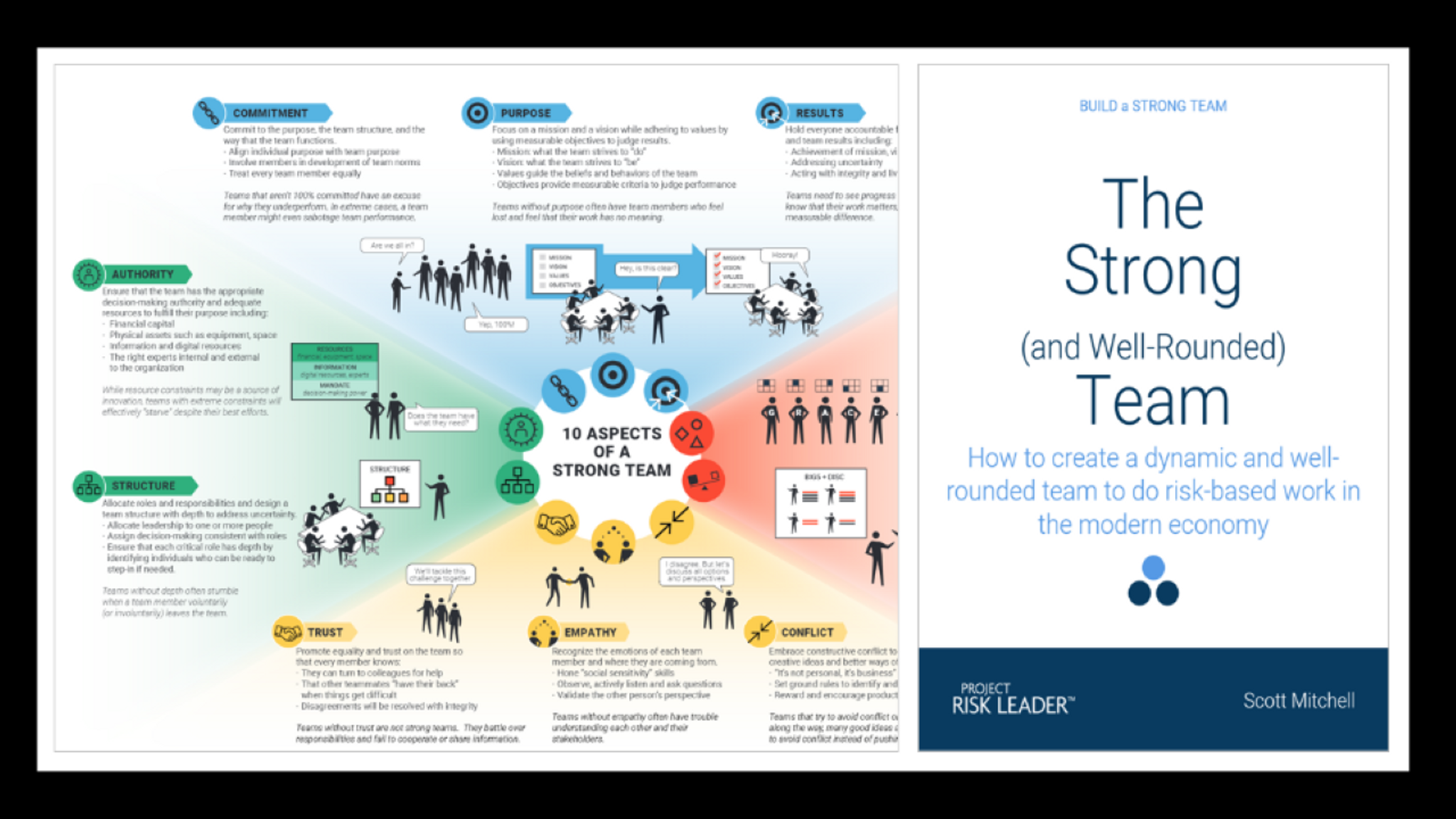

Build a Strong Team

The 10 Aspects of Strong Team detail evidence-based factors that increase the effectiveness and performance of teams doing risk-based work.

What are the 10 Aspects of a Strong Team

For over forty years, business leaders have worked to create a team model that accurately describes the traits of the most successful teams. Despite the value of these models, risk-based work requires a unique outlook.

The Strong and Well-Rounded Team

This eBook teaches you how to build a strong team to do risk-based work.

Overview of "The Winning Business Case"

Creating a winning business case for risk-related work requires "several arts and sciences" including those related to strategy, innovation, planning, financial analysis, narrative, media design, and persuasion. Use the step-by-step Winning Business Case Model to streamline your approach.

How to Build a Strong Business Case for Risk-Related Projects

The Winning Business Case Approach to building a business case details three phases with straightforward steps to help you make a strong business case and persuade your executives to do the right thing.

Making a Strong Business Case

Building a compelling business case is difficult. Building a compelling business case for risk-related projects can be even more difficult because some executives don’t naturally understand how this kind of work supports achievement of business objectives - they just view risk management as a cost center.